The tax structure of cigarettes in Bangladesh is more complex than in any other country in the world. Since the National Board of Revenue (NBR)’s revenue collection and monitoring system is not fully technology-driven, this multi-tier cigarette tax structure has become even more complicated. As a result, tobacco companies have more opportunities to evade taxes.

In particular, by increasing cigarette prices year after year without increasing taxes, policymakers have effectively allowed cigarette companies to earn continuous profits. Therefore, proposals to increase prices without raising taxes may appear to increase the burden on consumers, but in reality, they will allow tobacco companies to make huge profits. This would be highly counterproductive. As a tobacco control journalist, there is no scope to support any proposal that increases tobacco company profits. Because if companies’ profits increase, they will expand the business of death. Increased profits will also allow them to exert influence over government administration and other sectors.

What do international experts propose for tobacco control?

Like previous years, international experts have proposed cigarette tax and price increases for the upcoming fiscal year in Bangladesh. It is important to analyze how justified, realistic, and implementable their tax proposals are, and whether they will truly help tobacco control in Bangladesh.

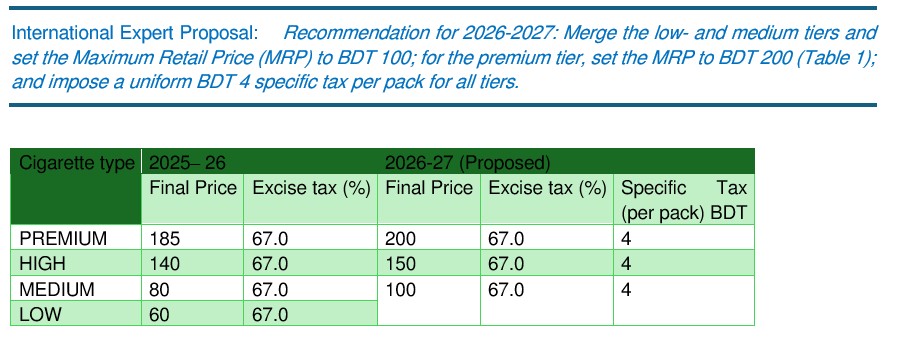

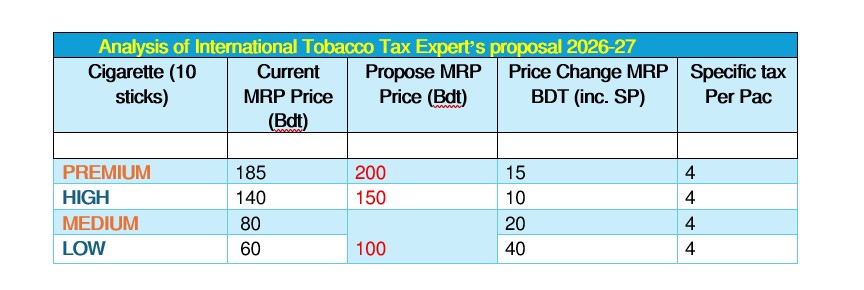

In Bangladesh, cigarettes are divided into four tiers based on price: premium, high, medium, and low. Among these, the most expensive cigarettes fall under the premium tier, where the price of a pack of 10 sticks is 185 BDT. The international experts have proposed increasing this to 200 BDT (an increase of 15 BDT) and introducing a specific tax of 4 BDT per pack.

Similarly, in the high tier, the price of a 10-stick pack is proposed to increase from 140 BDT to 150 BDT, with an additional 4 BDT specific tax.

In the medium tier, the current price of a pack is 80 BDT, proposed to increase to 100 BDT. Out of this 20 BDT increase, a 4 BDT specific tax is also proposed per pack. However, one of the most significant aspects of this proposal is the suggestion to merge the low and medium tiers into a single tier.

For discussion purposes, the proposal for the low tier is especially important, as this is the most widely sold cigarette segment in Bangladesh. The price of the most widely sold low-tier cigarettes is proposed to increase from 60 BDT to 100 BDT. As with other tiers, a 4 BDT specific tax per pack is proposed.

Ensuring price increases do not benefit tobacco companies

As mentioned earlier, Bangladesh’s multi-tier cigarette tax structure is highly complex, and the number of cigarette brands is also very high. Bangladesh is among the countries where the cheapest cigarettes are available. At the same time, cigarettes are sold everywhere—on streets, sidewalks, playgrounds, and in front of educational institutions. It is difficult to say how many countries have such a wide variety of cigarette brands.

Therefore, experiences, research, and practices from other countries cannot be directly applied here. Bangladesh’s cigarette market system, marketing structure, and supply chain—from companies to retailers—do not exist in many countries. As a result, while price increases will raise cigarette prices and increase revenue for the National Board of Revenue (NBR), the other side of the coin is that tobacco companies will also have opportunities to profit under this proposal by international tax experts.

For the first time, introducing a specific tax of 4 BDT per pack alongside the existing ad valorem tax system creates a mixed tax system in Bangladesh. However, the way this specific tax is proposed may lead to concerns about complexity and double taxation.

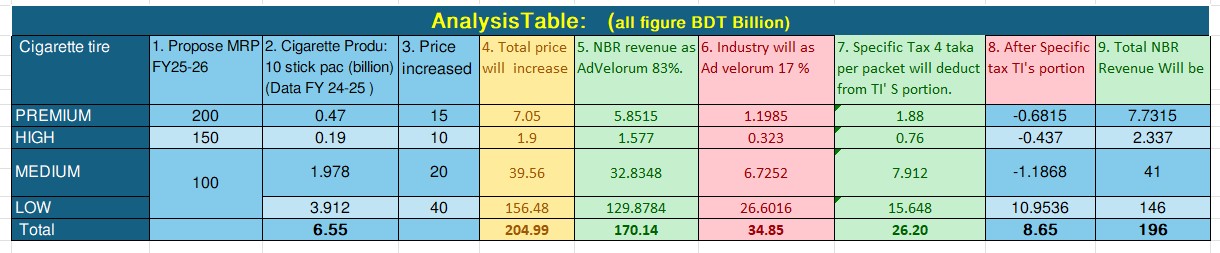

For example, in the premium tier, a 15 BDT price increase includes a 4 BDT specific tax per pack. According to NBR data, in the 2024–25 fiscal year, production in the premium tier was 4.65 billion sticks, which equals 0.47 billion packs (10 sticks per pack). With a 15 BDT increase, additional revenue from the premium tier would be approximately 7.05 billion BDT.

Out of this, under the ad valorem system (including supplementary duty, VAT, and health surcharge), the government would receive 83% or 5.85 billion BDT. The remaining 17% (approximately 1.19 billion BDT) would go to the cigarette companies as production cost and profit. Additionally, the government would collect 1.86 billion BDT as specific tax. Therefore, total additional government revenue from the premium tier would be 7.71 billion BDT, while the companies’ additional profit would decrease.

High Tier:

Similarly, in the high tier, 0.19 billion packs would generate an additional 1.90 billion BDT. The government would receive 1.57 billion BDT (83%), while companies would get 0.33 billion BDT. An additional 0.76 billion BDT would be collected as specific tax, reducing companies’ additional profit.

Medium Tier:

In the 2024–25 fiscal year, medium-tier production was 1.97 billion packs. A proposed 20 BDT price increase would generate 39.56 billion BDT in additional revenue. The government would receive 32.83 billion BDT (83%), companies 6.72 billion BDT (as production cost and profits including 17%), plus 7.88 billion BDT as specific tax. Thus, company profit would decrease.

Low Tier:

In the low tier, production was 3.91 billion packs. A 40 BDT price increase would generate 156.48 billion BDT. The government would receive 129.88 billion BDT (83%), companies 26.60 billion BDT (17%), plus 15.64 billion BDT as specific tax. Thus, company revenue would reduce to 10.96 billion BDT.

Revenue will increase by about 200 billion BDT, not 440 billion

Based on total production of 6.55 billion packs in 2024–25, the proposal would generate approximately 196 billion BDT in additional government revenue. In contrast, companies would earn about 8.65 billion BDT. Bangladesh’s cigarette market is about 77% controlled by British American Tobacco Bangladesh. In 2024, their after-tax net profit was 17.50 billion BDT. If the new proposal is implemented, their profits may increase further, and a large portion of it will go abroad. This would expand the tobacco business and pose greater risks to public health in the world’s eighth most populous country, Bangladesh.

Complications of double taxation

However, a major problem with the international experts’ proposal is the complexity of the tax structure, which may create challenges in implementation. The proposal suggests an 83% tax on the increased price first under the ad valorem system, followed by a 4 BDT specific tax per pack. This may create multiple layers of taxation, raising concerns.

To implement this system, the NBR would need to modify or add to its schedule, making the process more complex. Since tax would first be collected on the MRP, and then again as a specific tax, questions may arise about taxing already taxed amounts.

Proposal to increase price without increasing company profit

There is an alternative. A specific tax of 1 BDT per cigarette stick could be introduced. This would increase the price by 10 BDT per pack, and the entire amount would go to government revenue. This would increase prices for consumers, slightly reducing consumption.

If this policy is implemented, approximately 70 billion BDT in additional annual revenue could be generated. The price of cigarettes would increase, but company profits would not increase. At the same time, it would avoid the complications of double taxation.

Since cigarette production data is available to the government, collecting an additional One BDT per stick would not be difficult under a mixed system.

For example, if a 10-stick pack in the low tier currently costs 60 BDT, adding a 1 BDT tax per stick would increase the price to 70 BDT. Under the mixed system, the existing 83% tax would remain, and the additional 10 BDT would go directly to the government. Thus, there would be no confusion regarding double taxation.

Importance of local stakeholders

Government policy in Bangladesh is significantly influenced by tobacco companies. On the other hand, organizations working on tobacco control are also actively involved. Around 22 organizations are working on tobacco control in the capital alone. However, local stakeholders are often not adequately included in international proposals. This gap reduces the effectiveness of such proposals.

Conclusion

Effective tobacco control requires a simple, transparent, and strong tax structure. Price increases alone are not enough; policies must reduce consumption, increase government revenue, and limit tobacco company profits. Local experts must be involved before implementing international proposals.

Writer, Planning Editor, Ekattor Television and Tobacco Control Researcher

sinhasmp@yahoo.com